- “EVERY MOMENT IN BUSINESS happens only once. The next Bill Gates will not build an operating system. The next Larry Page or Sergey Brin won’t make a search engine. And the next Mark Zuckerberg won’t create a social network. If you are copying these guys, you aren’t learning from them.”

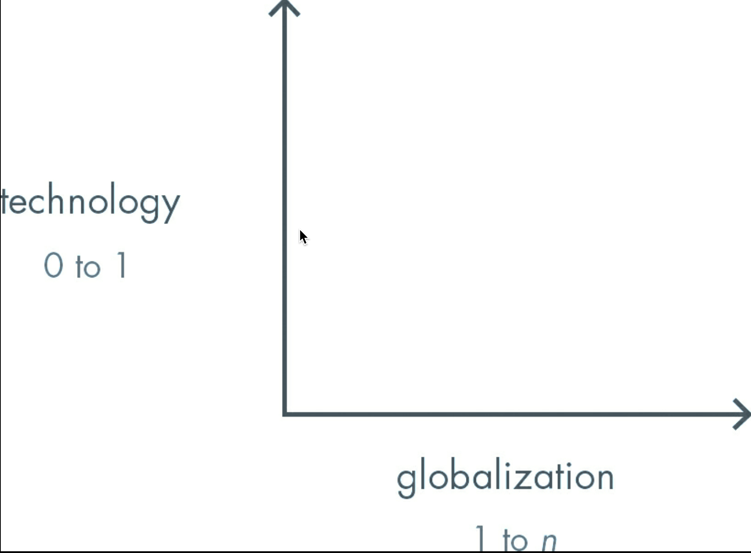

- “Of course, it’s easier to copy a model than to make something new. Doing what we already know how to do takes the world from 1 to n, adding more of something familiar. But every time we create something new, we go from 0 to 1. The act of creation is singular, as is the moment of creation, and the result is something fresh and strange.”

- “Technology is miraculous because it allows us to do more with less, ratcheting up our fundamental capabilities to a higher level. Other animals are instinctively driven to build things like dams or honeycombs, but we are the only ones that can invent new things and better ways of making them.”

- “The paradox of teaching entrepreneurship is that such a formula necessarily cannot exist; because every innovation is new and unique, no authority can prescribe in concrete terms how to be innovative. Indeed, the single most powerful pattern I have noticed is that successful people find value in unexpected places, and they do this by thinking about business from first principles instead of formulas.”

- Peter Thiel aruges that his vast experience in investing in co-founding and investing successful businesses have taught him that there is no formula for entrepreneurship. That is not what this book is about. If there’s something he learned about entrepreneurship, it is that entrepreneurs look in uncommon places for innovation and rely on first principles thinking. First principles thinking is breaking down complicated ideas into their most basic principles and you reassemble them from the ground up. First principles are assumptions or propositions that cannot be deduced from another assumption.

- “WHENEVER I INTERVIEW someone for a job, I like to ask this question: “What important truth do very few people agree with you on?””

- A good answer would first layout the truth that most people believe in, then explain your contrarian position.

- The quesiton above is important because it reveals propensity to changing the future and creating new things. While nobody can predict the future, we know two things about: it’s going to be rooted in today’s world and it’s going to be different. To the extent we can change things from what they are now, our future will occur closer than it otherwise would.

- There are two types of progress: horizontal progress which builds on things that already exist. If you have a typewriter and you build a 100, that is horizontal progress. Vertical progress is when you have a typewriter and you build a word processor. It is much harder to do because it requires thinking of something new, something that no ones has done before.

- At the macro level, the single word for horizontal progress is globalization: taking things that word in one part of the world and make them work everywhere. China has done this: they’ve copied western inventions, even though they may have skipped a few steps in the process – eg: leaping to wireless technology without first adopting a landline infrastructure.

There is one word associated with vertical progress: Technology. But there is no reason as to why technology should be just associated with computers. Properly understood, any vertical progress is technology.

- “To the contrarian question is that most people think the future of the world will be defined by globalization, but the truth is that technology matters more. Without technological change, if China doubles its energy production over the next two decades, it will also double its air pollution. If every one of India’s hundreds of millions of households were to live the way Americans already do—using only today’s tools—the result would be environmentally catastrophic. In a world of scarce resources, globalization without new technology is unsustainable.”

- Technology progress isn’t going to happen automatically, it is a result of deliberate work. Our ancestors lived in societies where a zero-sum game existed: they extracted resources from each other, and any creation of new resources rarely occurred. with the advent of steam-powered trains and industrial revolution, societies have started experiencing rapid technological progress and each generation was better off than the one before. This was the case until 1960s, 1970s. The technological progress since has occurred in the field of IT and computers. This is why it has become more difficult to continue progress at the same rate it was until the 70s and why we couldn’t achieve things such as four day workweek, vacations on the moon, etc.

- Startups work on the principle that you need other people to get stuff done, but at the same time the company needs to stay small enough to make this happens. Startups tend to come up with new technology. Almost impossible for one to do it – except if you’re an artist, or if you’re part of a large organization.

- A startup is the largest group of people you can put together to convince of a plan to build a better future: to rethink business from scratch and question received ideas.

- The question “tell me about a truth that you believe in which most people don’t” is difficult to answer directly. Instead, if you divide it into first finding something that most people agree on and which isn’t truthful can make the basis for you to then find the contrarian truth.

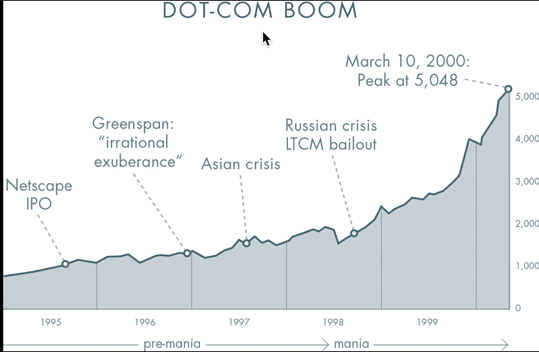

- The first step in creating a new technology is to question old assumptions. Old assumptions are only proven wrong in retrospect. Old and wrong assumptions could be widely adopted too: in the 1990s, and with the craze of the internet, page views became more important metric than the financial health of a company and its ability to turn profits. When these old beliefs collapse, the distortions that they created do not collapse immediately.

- A good way to understand the mania of the last 18months prior to the crash of 2000 is to understand the circumstances in the 90s. Yes, there was some optimism with the collapse of the Berlin wall but there were many other issues: questions about the US labor market competitiveness with manufacturing jobs going to Mexico. Questions about globalization and America’s role arose. Recovery from recession in the early 90s was slow. There was the asian financial crisis and also the Ruble crisis. All of that culminated in the mania of the late 90s where it was thought that internet is the way to move forward.

- With the dotcom bubble crash in 200s, investors pivoted back to bricks and away from clicks. Globalization was looked at as the way to progress since technology failed – investing in BRICs. This will eventually lead to the financial crisis. Those who stayed in tech have learned 4 lessons.

- Make incremental advances: talking about grand visions and long-term future success drew suspicion

- If your product needs advertising, you have the wrong product: focus instead on products that sell without marketing

- Improve on competition

- Stay lean and flexible

- “The most contrarian thing of all is not to oppose the crowd but to think for yourself”

- Companies that describe themselves as having no competitors need to make sure that they’re not defining their market too narrowly. Consider the situation where you’d want to open a British restaurant in an area because you have determined that there are no other British restaurants in that area. But what if your competition is other restaurants in the area, not just British ones?

- It would be wise to determine whether there are people who would rather have British food above all else. Do not fall the temptation of telling yourself how you’re different from most of the restaurants that end up out of business within 2 years of opening.

- “If you lose sight of competitive reality and focus on trivial differentiating factors—maybe you think your naan is superior because of your great-grandmother’s recipe—your business is unlikely to survive.”

- Non-monopolists exaggerate their distinction by defining their market as the intersection of small marketsb

British food ^restaurant ^ Palo Alto - Monopolists disguise their monopoly by framing it as the union of large marekts

Search U consumer electronics U ads - Businesses that operate in a very competitive space will almost always focus on survival. If you are one of the restaurants in the Silicon Valley, you might try to differentiate yourself by offering good food at reasonable prices, driving you to look for efficiencies wherever possible: employing people only at minimum wage and putting grandma to help at the cashier. Companies that have the latitude of monopoly can offer to care about things beyond survival and money, and that is why it can offer employees competitive wages and better working conditions.

- Is monopoly good for the company but bad externally, for society? the answer is yes as long as the state of society isn’t changed by other disruptive monopolies.

In a world where societies remain the same, monopolies become like rent collectors: people have to pay their rent and the deed may shuffle. History shows us though that monopolies didn’t lead to the society entering a stasis status. Other monopolies replaced the incumbents. Apple mobile devices replaced Microsoft OS dominance that happened for decades – and MS replaced the world’s dependence on IBM’s hardware before that. Monopolies create greater abundance, not artificial scarcity. This is why people were happy to pay monopolies extra money because they finally had the option to get a good smartphone like the iPhone. - The whole idea that competition is the desired status will result in society entering a state of stasis and ultimately death. The state of equilibrium is what is governing most of the universe but in a state of equilibrium, your business will easily be replaced by some other undifferentiated business. Equilibrium isn’t the state where new creations take place.

- The concept of competition is ingrained in our societies. We see it in our educational system where students compete to get a higher grade in a largely cookie-cutter system that punishes students who can’t perform well in a setting that requires them to sit still on a desk for hours daily. Peter recall his high-school days where it was clearly predicated that he will get into Stanford. After graduation and getting into law school, the goal of hundreds of thousands of students was to compete for a Supreme Court clerkship. Peter did, and he got into the final interviews for a clerkship position with Justices Scalia and Kennedy. He was devastated when things didn’t work but couldn’t have been happier 10 years later from then as was leading PayPal and actually creating new things as opposed to reading drafts of new things that other people created.

- “More than anything else, competition is an ideology—the ideology—that pervades our society and distorts our thinking. We preach competition, internalize its necessity, and enact its commandments; and as a result, we trap ourselves within it—even though the more we compete, the less we gain”

- “For the privilege of being turned into conformists, students (or their families) pay hundreds of thousands of dollars in skyrocketing tuition that continues to outpace inflation. Why are we doing this to ourselves?”

- Thiel believes that competition is distracting and can make businesses miss the elephant room: you are so focused on beating your competition, copying them and getting ahead of them that you lose sight as to whether what you’re doing is really worth doing. To put it into an analogy, winning a war is inconsequential if the war isn’t worth fighting in the first place, because all participants end up becoming losers. Look at what Microsoft and Google did: Bing to compete with Google, Chrombook and Surface Pro, Windows and Chrome OS. Competition ignites this feeling of the need to beat competitors and even uses war terms in business context: sales force, captive market, make a killing, and headhunters.

- “Inside a firm, people become obsessed with their competitors for career advancement. Then the firms themselves become obsessed with their competitors in the marketplace. Amid all the human drama, people lose sight of what matters and focus on their rivals instead”

- “Rivalry causes us to overemphasize old opportunities and slavishly copy what has worked in the past. Consider the recent proliferation of mobile credit card readers. In October 2010, a startup called Square released a small, white, square-shaped product that let anyone with an iPhone swipe and accept credit cards. It was the first good payment processing solution for mobile handsets. Imitators promptly sprang into action.”

- If you’re less sensitive to social cues, you’re less likely to do the same things as everyone else around you.

- “Competition can make people hallucinate opportunities where none exist. The crazy ’90s version of this was the fierce battle for the online pet store market. It was Pets.com vs. PetStore.com vs. Petopia.com vs. what seemed like dozens of others. Each company was obsessed with defeating its rivals, precisely because there were no substantive differences to focus on. Amid all the tactical questions—Who could price chewy dog toys most aggressively? Who could create the best Super Bowl ads?—these companies totally lost sight of the wider question of whether the online pet supply market was the right space to be in. Winning is better than losing, but everybody loses when the war isn’t one worth fighting.”

- Soemtimes in business you do have to fight, if you decide to fight you can’t go half way: you’ll have to fight quick and hit hard to win. Otherwise, do not fight.

- The value of a tech business is the sum of all discounted future cash flows. It takes time to build a successful business. This is why successful tech businesses tend to lose money in the first 10-15 years of their lifecycle. Traditional businesses that face competition do have their revenues decline over time and that is why they have a market value lower than tech startups.

- “LinkedIn is another good example of a company whose value exists in the far future. As of early 2014, its market capitalization was $24.5 billion—very high for a company with less than $1 billion in revenue and only $21.6 million in net income for 2012. You might look at these numbers and conclude that investors have gone insane. But this valuation makes sense when you consider LinkedIn’s projected future cash flows.”

- Humans tend to b hyper-focused on growth and have a hard time wrapping their heads around durability. They follow metrics like average daily users, time spent in app, quarter over quarter revenues. Yet, you can still hit these numbers while these numbers don’t really tell the story of whether the business will continue to exist a decade from now. This was the story of Groupon and Zynga. Groupon experienced an explosive growth short term but realized how hard it is to get their initial hundreds of thousands of clients to re-sign with them.

- “If you focus on near-term growth above all else, you miss the most important question you should be asking: will this business still be around a decade from now? Numbers alone won’t tell you the answer; instead you must think critically about the qualitative characteristics of your business.”

- To assess the ability of a business to be monopolistic, you’ll need to think about whether it has the following: proprietary technology, network effects, economies of scaling and branding. This isn’t a list of boxes to check as you build your business- there’s no shortcut to monopoly. However, it is helpful to think about your business from these dimensions as you build it.

- Technology proprietorship: This is the most important element in ensuring that you’ve got a monopoly. Extremely hard to replicate. Could come in multiple flavors: either you invent something new that wasn’t there before such as a cure to baldness or a way to skip sleep altogther and safely or it could be making significant 10x improvements to the next best competitor out there. Paypal offered a near instantaneous way of transmitting money, facilitating ecommerce transactions instead of posting cheques and transferring money through banks. Amazon offered the most comprehensive set of books available anywhere in the world – more than any other bookstore out there that it labeled itself the world’s largest bookstore.

- Network effect: increases the likelihood that other people will start using the product. If all your friends are on facebook, it would make sense for you to join. Joining another social network site where you’re the only one would make you an eccentric. Ensure though that your product is useful for the first set of few users who have it before the network effect proliferates. Xanadau was a company that was founded in the 1960s and had what could be thought of as an earlier version of the World Wide Web. They kept trying until they folded in the early 90s just as the World Wide Web was gaining prominence. Their issue was that they required all computers to join their network simultaneously in order for their solution to work. The first few users never benefited from it.

Paradoxically, businesses who want to have a network effect must start out small. Facebook started by just having people in Harvard join it. Mark’s goal wasn’t to have all people on earth join facebook. - Economies of scale: refers to the ability to spread fixed costs over greater quantities of sale. Software companies especially enjoy that as their costs of making the next copy of software is close to zero. Many businesses gain only limited advantage – if any, as they grow. Service business are specially difficult to scale. Yoga studios’ profits will remain fairly consistent even if you expand to different locations because the instructors that you have in one location cannot give classes to millions of people – engineers can create softwares that millions can.

- Branding: by definition, a company brand is proprietary. However, a business needs to take steps to make the brand synonym with the value the company creates. Take for example apple: their omnipresent ads, their uniquely-designed stores with their sleek minimalist look, and their premium materials that make them command a premium price associated with their brands.

Do not copy the skin and leave the substance. Many companies tried to copy the minimalist, premium-looking packaging, ads, and flashy keynotes that Apple has but failed. Because apple has a strong technology proprietorship underneath the flashy skin – superior touchscreen technology and software built specifically for that superior technology. Network effect where developers are incentivized to develop apps on the apple marketplace because that is where millions of use are. Also the economies of scale meant that it had price bargaining power with suppliers - Building a monopoly starts with technology proprietorship, network effect, economies of scale and branding, but you must choose your target market carefully. You almost always want to start with a small target market. Always err on the side of starting too small. This is easier to dominate. Make sure that a market does exist though. When Paypal came up with its initial market, it was based on the premise that Palm users could beam money into each other. This was a proprietary technology but people who used Palm were spread all over the world and so there was no people who wanted to use Paypal. This when Paypal pivoted into ebay auctions and focused on a few thousand powersellers who were doing lots of transactions through ebay. This was much better than trying to get millions of scattered people to use Paypal.

- The focus for a startup in terms of an initial target market is a few thousands of concentrated individuals who are currently served by few or no competitors. Targeting too wide a market is never a good idea. It is hard and it will bring competition if there isn’t already. This is why it is a redflag when an entrepreneur speaks about capturing 1% of a 100billion market.

Amazon is a textbook example of how to do that successfully. Jeff Bezos vision was to dominate online retail but he deliberately started with just books: easy to ship and allowed Amazon to have the competitive advantage of selling books where bookstores weren’t found or sell rare-to-find books. From there, Amazon had two choices: either expand the set of people who read books or slowly move into adjacent markets. They chose the latter and started selling CDs and Software. This trend continued until today. - sometimes, there are obstacles to scaling which is something that eBay had to find out about the hard way back in 2014. The auction model worked well for items like collector stamps but it turned out that people didn’t want to bid on Kleenex or other items. They just bought them quickly from Amazon. eBay is a valuable company, just not as valuable as it was once thought back in 2004.

- As you craft a plan to expand to adjacent markets, do not disrupt and avoid competition. Disruption could get you the wrong kind of attention. Napster disrupted the recording industry back in 1999. A year later, the founders were featured on the Time magazine. A year and a half later, they were in bankruptcy court. They directly challenged their big competitors. The focus shouldn’t be disruption. It should be focusing on creating something new.

- “startups’ obsession with disruption means they see themselves through older firms’ eyes. If you think of yourself as an insurgent battling dark forces, it’s easy to become unduly fixated on the obstacles in your path. But if you truly want to make something new, the act of creation is far more important than the old industries that might not like what you create. Indeed, if your company can be summed up by its opposition to already existing firms, it can’t be completely new and it’s probably not going to become a monopoly.”

- There is no strategic benefit to being the first mover: it should be a tactic not an end goal in and of itself. It is much better to be the last mover but with a plan to monopolize. Start with a niche small segment of the market to carry out your big vision. You begin with the end goal in mind. What matters is generating future cash flows, so there’s no value in you being the first mover if someone else is going to come an unseat you.

- How much does luck matter in the success of a startup? Peter isn’t sure of the answer but he believes that we are in an environment that unduly overestimates the role of luck and underrate the possibility of focusing on becoming exceptionally great one thing and achieving that outcome.

- He mentions how great entrepreneurs like Bezos and Gates talk about the role that luck played in their achievements

- Yet, he questions how luck could be the main factor since hundreds of successful serial entrepreneurs proceeded to create multiple and successful big businesses such as Musk and Jobs.

- He decries an education system that is focused on having students plan for a future of different possibilities and learn so many varying topics without being really ready for anything specific in a big way.

- Peter describes 4 schools of thoughts when it comes to the future- depending on whether you expect the future to be better or worse than now:

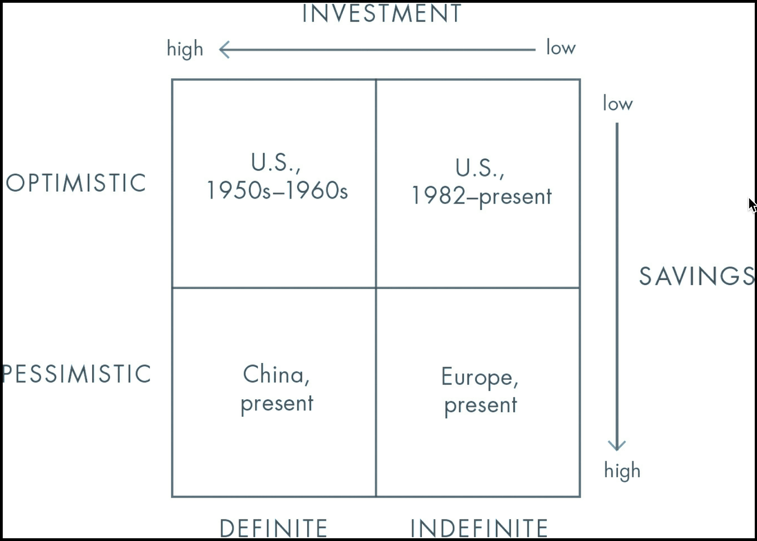

- indefinite pessimism: You can’t really change the fact that the worse is yet to come. You’re just not sure when and how it will occur. You don’t know what to do about the bleak future that is yet to come. This is how Europe has been since the 1970s, so they might as well vacation.

- Definite pessimism: You think the future can be known but you are certain that the future is going to be bleak, so it ends up dictating your current actions. This summarizes the situation in China: China has been achieving remarkable growth since the 2000s, yet: rich people are always trying to find ways to get their capital out of china. The poor are saving for when the day will come when things aren’t good, and the chinese leadership has lived through famine before and are in constant fear of it coming back. Yet, from the lens of the US – indefinite optimists, we think that things are good there.

- Indefinite Optimism: this has been the US since the 1970s onwards. It is a generation of people who experienced in the first 18 years of their lives great fortunes and improved economic situation year after year without much work they did on their own to make that happen. They just assume that this will continue, not sure how but they just assume it.

- Definite Optimism: Believes that the future can be known and can be better if you plan for it to be that way. This was the US between the 1870 to 1970 and Europe during the scientific revolution. Even during the Great Recession, the Empire State Building was completed in 2 years – between 1929 to 1931, the Golden Bridge, and the Manhattan project, and the interstate highway. People entertained audacious ideas seriously regardless of their source – eg: a highschool teacher proposing a huge infrastructure project in the US West Coast.

- “Indefinite attitudes to the future explain what’s most dysfunctional in our world today. Process trumps substance: when people lack concrete plans to carry out, they use formal rules to assemble a portfolio of various options. This describes Americans today. In middle school, we’re encouraged to start hoarding “extracurricular activities.” In high school, ambitious students compete even harder to appear omnicompetent. By the time a student gets to college, he’s spent a decade curating a bewilderingly diverse résumé to prepare for a completely unknowable future. Come what may, he’s ready—for nothing in particular.

Instead of pursuing many-sided mediocrity and calling it “well-roundedness,” a definite person determines the one best thing to do and then does it. Instead of working tirelessly to make herself indistinguishable, she strives to be great at something substantive—to be a monopoly of one. This is not what young people do today, because everyone around them has long since lost faith in a definite world. No one gets into Stanford by excelling at just one thing,” - “A definite pessimist believes the future can be known, but since it will be bleak, he must prepare for it. Perhaps surprisingly, China is probably the most definitely pessimistic place in the world today. When Americans see the Chinese economy grow ferociously fast (10% per year since 2000), we imagine a confident country mastering its future. But that’s because Americans are still optimists, and we project our optimism onto China. From China’s viewpoint, economic growth cannot come fast enough. Every other country is afraid that China is going to take over the world; China is the only country afraid that it won’t. China can grow so fast only because its starting base is so low. The easiest way for China to grow is to relentlessly copy what has already worked in the West. And that’s exactly what it’s doing: executing definite plans by burning ever more coal to build ever more factories and skyscrapers. But with a huge population pushing resource prices higher, there’s no way Chinese living standards can ever actually catch up to those of the richest countries, and the Chinese know it. This is why the Chinese leadership is obsessed with the way in which things threaten to get worse. Every senior Chinese leader experienced famine as a child, so when the Politburo looks to the future, disaster is not an abstraction. The Chinese public, too, knows that winter is coming. Outsiders are fascinated by the great fortunes being made inside China, but they pay less attention to the wealthy Chinese trying hard to get their money out of the country.”

- Biotech startups have more complex problems to solve than tech startups. Biotech companies work in an indefinite environment – natural biology. We didn’t design our bodies, and the more we learn about them, the more complex they turn out to be. Tech companies, on the other hand, work on a defined problem that is created in an artificial environment – easier to control. The proof is in the pudding: returns on investment in biotechnology have been steady decreasing – Eroom’s law

- “But today it’s possible to wonder whether the genuine difficulty of biology has become an excuse for biotech startups’ indefinite approach to business in general. Most of the people involved expect some things to work eventually, but few want to commit to a specific company with the level of intensity necessary for success. It starts with the professors who often become part-time consultants instead of full-time employees—even for the biotech startups that begin from their own research. Then everyone else imitates the professors’ indefinite attitude. It’s easy for libertarians to claim that heavy regulation holds biotech back—and it does—but indefinite optimism may pose an even greater challenge for the future of biotech.”

- Individuals in America today almost save nothing while corporations have a lot of money but do not have concrete plans to spend it. The government has turned form an entity that crafted strategies for groundbreaking projects- lunar exploration to a provider of insurance – medicaid and a dizzying array of transfer payments.

- Definite optimism works when you build the future you envision. Definite pessimism works by copying what is working without innovating. Indefinite pessimism becomes a self-fulfilling prophecy since you’re a slacker and have low expectations.

- Indefinite optimism seems unsustainable: how can anyone achieves a better future if no one plans for it? many draw a parallel from Darwinian evolution to suggest that indefinite optimism has its way of work, much like the fittest survives and evolves in the biological world without any definitive planning. Yet, is it fair to assume that the model of evolution that holds true in the biological world will hold true in other fields? after all, Newtonian physics doesn’t help explain Big Bang Theory or Black Holes.

It is not clear how Darwinism can explain how to build a better society or build a business out of nothing. - Design is extremely important when it comes to Products. Everyone wants to be a designer. One could aruge that Steve Jobs fretted over the design of the devices Apple created. While that is true, Steve’s biggest accomplishment was designing his business, especially crafting a long-term plan which is very difficult in a short-term thinking world. And this is why it is especially difficult to value privately-held companies. Entrepreneurs who have a definitive long-term plan will not sell their business. Companies wanting to buy strartups will likely misprice the business: they either overpay or underpay.

- “In 1906, economist Vilfredo Pareto discovered what became the “Pareto principle,” or the 80-20 rule, when he noticed that 20% of the people owned 80% of the land in Italy—a phenomenon that he found just as natural as the fact that 20% of the peapods in his garden produced 80% of the peas. This extraordinarily stark pattern, in which a small few radically outstrip all rivals, surrounds us everywhere in the natural and social world. The most destructive earthquakes are many times more powerful than all smaller earthquakes combined. The biggest cities dwarf all mere towns put together. And monopoly businesses capture more value than millions of undifferentiated competitors.”

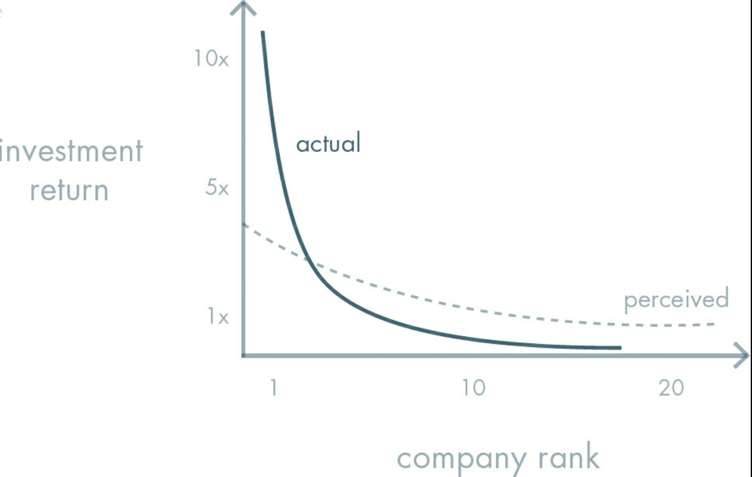

- Most VCs will take a few years until they’re successful, and most of them will never be. One of the mistakes committed by them is to assume that the negative returns generated by bad investment will be offset by positive returns in good companies. The issue is that a disproportionate percentage of the returns in the VC space are generated by a few investments. See graph below that demonstrates reality vs expectations:

- “The kind of portfolio thinking embraced by both folk wisdom and financial convention, by contrast, regards diversified betting as a source of strength. The more you dabble, the more you are supposed to have hedged against the uncertainty of the future. But life is not a portfolio: not for a startup founder, and not for any individual. An entrepreneur cannot “diversify” herself: you cannot run dozens of companies at the same time and then hope that one of them works out well. Less obvious but just as important, an individual cannot diversify his own life by keeping dozens of equally possible careers in ready reserve.”

- “People who understand the power law will hesitate more than others when it comes to founding a new venture: they know how tremendously successful they could become by joining the very best company while it’s growing fast. The power law means that differences between companies will dwarf the differences in roles inside companies. You could have 100% of the equity if you fully fund your own venture, but if it fails you’ll have 100% of nothing. Owning just 0.01% of Google, by contrast, is incredibly valuable.

If you do start your own company, you must remember the power law to operate it well. The most important things are singular: One market will probably be better than all others, as we discussed in Chapter 5. One distribution strategy usually dominates all others, too—for that see Chapter 11. Time and decision-making themselves follow a power law, and some moments matter far more than others—see Chapter 9.”

- “All fundamentalists think this way, not just terrorists and hipsters. Religious fundamentalism, for example, allows no middle ground for hard questions: there are easy truths that children are expected to rattle off, and then there are the mysteries of God, which can’t be explained. In between—the zone of hard truths—lies heresy. In the modern religion of environmentalism, the easy truth is that we must protect the environment. Beyond that, Mother Nature knows best, and she cannot be questioned. Free marketeers worship a similar logic. The value of things is set by the market. Even a child can look up stock quotes. But whether those prices make sense is not to be second-guessed; the market knows far more than you ever could. Why has so much of our society come to believe that there are no hard secrets left? It might start with geography. there are no spaces left on the map anymore. If you grew up in the 18th century, there were still new places to go…Today, explorers are found mostly in history books and children’s tales.”

- “Along with the natural fact that physical frontiers have receded, four social trends have conspired to root out belief in secrets. First is incrementalism. From an early age, we are taught that the right way to do things is to proceed one very small step at a time, day by day, grade by grade. If you overachieve and end up learning something that’s not on the test, you won’t receive credit for it. But in exchange for doing exactly what’s asked of you (and for doing it just a bit better than your peers), you’ll get an A.

- Second is risk aversion. People are scared of secrets because they are scared of being wrong.By definition, a secret hasn’t been vetted by the mainstream. If your goal is to never make a mistake in your life, you shouldn’t look for secrets. The prospect of being lonely but right—dedicating your life to something that no one else believes in—is already hard. The prospect of being lonely and wrong can be unbearable.

- Third is complacency. Social elites have the most freedom and ability to explore new thinking, but they seem to believe in secrets the least. Why search for a new secret if you can comfortably collect rents on everything that has already been done?

- Fourth is “flatness.” As globalization advances, people perceive the world as one homogeneous. Given that assumption, anyone who might have had the ambition to look for a secret will first ask himself: if it were possible to discover something new, wouldn’t someone from the faceless global talent pool of smarter and more creative people have found it already?

- There’s an optimistic way to describe the result of these trends: today, you can’t start a cult. Forty years ago, people were more open to the idea that not all knowledge was widely known. From the Communist Party to the Hare Krishnas, large numbers of people thought they could join some enlightened vanguard that would show them the Way. Very few people take unorthodox ideas seriously today, and the mainstream sees that as a sign of progress. Yet, it has come at a cost: we have given up our sense of wonder at secrets left to be discovered.”

- There are still secrets left in the world to be discovered. Take for example social injustices. If there were no secrets left, we’d be having a perfectly just society. Back in time, a few regarded slavery as injust – and rightly so. It took time for that view to become mainstream. Besides, eventual decline will be what ensues when an entity stops believing in secrets. The decline of HP in the period of the early 2000s is a perfect illustration of that: it merged with Compaq – cz it had no better ideas, and released a consulting/support service which was not innovative.

- “The same reason that so many internet companies, including Facebook, are often underestimated—their very simplicity—is itself an argument for secrets. If insights that look so elementary in retrospect can support important and valuable businesses, there must remain many great companies still to start.”

- “Beginnings are special. They are qualitatively different from all that comes afterward. This was true 13.8 billion years ago, at the founding of our cosmos: in the earliest microseconds of its existence, the universe expanded by a factor of 1030—a million trillion trillion. As cosmogonic epochs came and went in those first few moments, the very laws of physics were different from those we know today. It was also true 227 years ago at the founding of our country: fundamental questions were open for debate by the Framers during the few months they spent together at the Constitutional Convention. How much power should the central government have?

- after ratifying the Bill of Rights in 1791, we’ve amended the Constitution only 17 times. Today, California has the same representation in the Senate as Alaska, even though it has more than 50 times as many people. Maybe that’s a feature, not a bug. But we’re probably stuck with it as long as the United States exists. Another constitutional convention is unlikely;

- Companies are like countries in this way. Bad decisions made early on—if you choose the wrong partners or hire the wrong people, for example—are very hard to correct after they are made. It may take a crisis on the order of bankruptcy before anybody will even try to correct them. As a founder, your first job is to get the first things right, because you cannot build a great company on a flawed foundation.”

- “Now when I consider investing in a startup, I study the founding teams. Technical abilities and complementary skill sets matter, but how well the founders know each other and how well they work together matter just as much. Founders should share a prehistory before they start a company together—otherwise they’re just rolling dice.”

- ” To anticipate likely sources of misalignment in any company, it’s useful to distinguish between three concepts:

Ownership: who legally owns a company’s equity?

Possession: who actually runs the company on a day-to-day basis?

Control: who formally governs the company’s affairs?

A typical startup allocates ownership among founders, employees, and investors. The managers and employees who operate the company enjoy possession. And a board of directors, usually comprising founders and investors, exercises control. In theory, this division works smoothly. but it also multiplies opportunities for misalignment. To see misalignment at its most extreme, just visit the DMV. Suppose you need a new driver’s license. Theoretically, it should be easy to get one. The DMV is a government agency, and we live in a democratic republic. All power resides in “the people,” who elect representatives to serve them in government. If you’re a citizen, you’re a part owner of the DMV and your representatives control it, so you should be able to walk in and get what you need. Of course, it doesn’t work like that. We the people may “own” the DMV’s resources, but that ownership is merely fictional. The clerks and petty tyrants who operate the DMV, however, enjoy very real possession of their small-time powers. Even the governor and the legislature charged with nominal control over the DMV can’t change anything. The bureaucracy lurches ever sideways of its own inertia no matter what actions elected officials take. Accountable to nobody, the DMV is misaligned with everybody. Bureaucrats can make your licensing experience pleasurable or nightmarish at their sole discretion. You can try to bring up political theory and remind them that you are the boss, but that’s unlikely to get you better service.” - To prevent misalignments especially at the early stages of a startup, keep your board of directors small, between 3-5. Also, ensure that anyone who does work for the company is either salaried or has ownershiop of the company. Consultants might be focused on near-term accomplishments.

- “For people to be fully committed, they should be properly compensated. Whenever an entrepreneur asks me to invest in his company, I ask him how much he intends to pay himself. A company does better the less it pays the CEO—that’s one of the single clearest patterns I’ve noticed from investing in hundreds of startups. In no case should a CEO of an early-stage, venture-backed startup receive more than $150,000 per year in salary. It doesn’t matter if he got used to making much more than that at Google”

- If a CEO pays themselves a lot, they risk becoming like politicans instead of founders: they will start defending the current status quo instead of thinking outside-of-the-box to create value. In addition, the CEO salary sets precedent for those employees joning the company: a low CEO salary signals long-term commitment from the CEO that employees will emulate – and vice-versa.

- Equity isn’t the perfect way to create incentives but it’s a good way to ensure broad alignment with the company’s long-term goals. Do not reveal what stake each person has: Giving people equal amount of shares seems unfair and giving them uneuqal amounts at the beginning will seem unfair too. A secretary who joins the company early on might get more in equity value than those who play a crucial role in the success of the company later on.

- It is not only important for a startup that you pick talented people from a pile of resumes, it is important that these individuals enjoy the time they spend together and are inclined to interact with one another outside of work. “If you can’t count durable relationships among the fruits of your time at work, you haven’t invested your time well—even in purely financial terms.”

- Hiring should never be outsourced. You need to screen candidates beyond the core set of competencies required of them to do the job. Do not rely on perks to attract candidates: A candidate who is swayed by extra perks isn’t someone you want on your team. Instead focus on identifying why a great candidate who could easily be hired by Google would instead choose to work for your company and be the 20th employee. Usually, you should be able to sell them your company based on the specifics of your mission and the team/people they’ll be working with.

“You can’t be like the Google of 2021 in terms of compensation or perks, but you can be like the Google of 1999 in terms of mission and team.” - In the early phases of a startup, focus on making the team unique to the people on the outside but have something that unifies them in the inside. Give each employee unique responsibilities to avoid clashes internally.

- “You may think that you’re an exception; that your preferences are authentic, and advertising only works on other people. It’s easy to resist the most obvious sales pitches, so we entertain a false confidence in our own independence of mind. But advertising doesn’t exist to make you buy a product right away; it exists to embed subtle impressions that will drive sales later. Anyone who can’t acknowledge its likely effect on himself is doubly deceived.”

- “You may think that you’re an exception; that your preferences are authentic, and advertising only works on other people. It’s easy to resist the most obvious sales pitches, so we entertain a false confidence in our own independence of mind. But advertising doesn’t exist to make you buy a product right away; it exists to embed subtle impressions that will drive sales later. Anyone who can’t acknowledge its likely effect on himself is doubly deceived.”

- “Nerds are used to transparency. They add value by becoming expert at a technical skill like computer programming. In engineering disciplines, a solution either works or it fails. You can evaluate someone else’s work with relative ease, as surface appearances don’t matter much. Sales is the opposite: an orchestrated campaign to change surface appearances without changing the underlying reality. This strikes engineers as trivial if not fundamentally dishonest. They know their own jobs are hard, so when they look at salespeople laughing on the phone with a customer or going to two-hour lunches, they suspect that no real work is being done. If anything, people overestimate the relative difficulty of science and engineering, because the challenges of those fields…”

- “Like acting, sales works best when hidden. This explains why almost everyone whose job involves distribution—whether they’re in sales, marketing, or advertising—has a job title that has nothing to do with those things. People who sell advertising are called “account executives.” People who sell customers work in “business development.””

- “Whatever the career, sales ability distinguishes superstars from also-rans. On Wall Street, a new hire starts as an “analyst” wielding technical expertise, but his goal is to become a dealmaker. A lawyer prides himself on professional credentials, but law firms are led by the rainmakers who bring in big clients.”

- “The most fundamental reason that even businesspeople underestimate the importance of sales is the systematic effort to hide it at every level of every field in a world secretly driven by it.”

- “The engineer’s grail is a product great enough that “it sells itself.” But anyone who would actually say this about a real product must be lying: either he’s delusional (lying to himself) or he’s selling something (and thereby contradicting himself). The polar opposite business cliché warns that “the best product doesn’t always win.” Economists attribute this to “path dependence”: specific historical circumstances independent of objective quality can determine which products enjoy widespread adoption.That’s true, but it doesn’t mean the operating systems we use today and the keyboard layouts on which we type were imposed by mere chance. It’s better to think of distribution as something essential to the design of your product. If you’ve invented something new but you haven’t invented an effective way to sell it, you have a bad business—no matter how good the product.”

- When the size of the deal gets big, navigating the politics and nurturing the relationships to make the deal become very important. Alex Karp, the co-founder of Palantir, spends 28 days on the road talking to clients. The potentital deal size is anywhere between 1-100mill, you want sales to becom invisibile. Plus, companies want to talk to the CEO at that size of deal not the VP. Also, your first client might become your biggest client but you can’t hit them with the biggest contract from the get go. You’ll have to get some clients under your belt before starting to land bigger deals.

- Thiel believes that there exists a zone between products that can be sold through viral marketing – requires no personal intervention, and those that do. An example could be a product that you’d design for convenience store owners. If that product would sell for 1000, you’d need a sales associate to sell it, yet it would be too expensive to hire a sales associate to sell it. And you also cannot sell it by advertising just to convenience store owners.

“This is why so many small and medium-sized businesses don’t use tools that bigger firms take for granted. It’s not that small business proprietors are unusually backward or that good tools don’t exist: distribution is the hidden bottleneck.”

- A product is viral if users invite others to use it – eg: facebook and paypal. This way, user acquisition is both cheap and fast.

- The 7 Questions that are essential for every new company’s success. These were the questions that were invariably ingored by mainly failed green tech companies in post 08 recesssion

- Are you breaking new grounds instead of making incremental improvements?

You need to develop something new that is 2x to 10x better than nearest substitute.

Tesla’s Answer: Tesla’s technology was superior on all fronts. Other car manufacturers relied on it – Mercedes, Toyota, GM. Not only that, but the sum of Tesla’s technological superiority was greater than its parts. Tesla consistently ranked higher than any other car. - Can you capture a significant portion of a small market segment to start with?

Do you have the small market that you want to capture clearly defined? or do you shift the market size that you’re targeting depending on whether the discussion is about the opportunity that exists for your business – you increase the market size here to exaggerate the potential, or reduce it – when you want to describe the strength that your company has.

Tesla’s answer: They started with a small segment: electric roadsters, and that allowed them to have the funds ready to do research to create other models, and also to appeal to people who wanted to be environmentally conscious in this segment. - Do you have the right team?

Tesla’s answer: Musk described working at Tesla as being part of a “special force”. - Do you have a clearly defined plan to distribute – market and sell, the product and not just make it?

Selling and distributing the product is at least as important as creating it.

Tesla’s answer: Tesla took distribution very seriously. While other manufacturers let dealers sell their cars – the cheaper approach upfront, Tesla sold and serviced their cars through their own chain and eventhough that meant higher costs upfront, it meant lower costs in the long term and more brand affinity from customers - Can you defend your moat for 10-20 years?

Ask yourself what will the world look like 10-20 years from now and how will you defend your position then? one of the big failures of cleantech in the 2010s was to blame Chinese Solar manufacturers for their failings. The government even backed them up. However, was the Chinese challenge to their business hard to foresee? - Have you identified an opportunity that others do not see

Are you just capitalizing on a general trend that lots of companies are jockeying on or is there a specific reason that makess your company different from others,? reasons you see but others do not?

Tesla’s answer: Tesla understood that rich people wanted to appear to be environmentally conscious even if it meant driving boxy cars. Tesla created cool cars that are environmentally conscious and are of superior quality. - Is this is the right time to start your business?

Are you objective about the developments that exist at the moment you want to start a business and which would make your business unique, or is that uniqueness just perceived?

Tesla’s answer: Musk spotted a one-in-a-lifetime opportunity unlike competitors who thought that federal subsidies will be provided indefinitely in 2010. He grabbed access to a ~.5 billion dollar loan knowing tht this is the moment to seize.

- Are you breaking new grounds instead of making incremental improvements?

- “Doing something different is what’s truly good for society—and it’s also what allows a business to profit by monopolizing a new market. The best projects are likely to be overlooked, not trumpeted by a crowd; the best problems to work on are often the ones nobody else even tries to solve.”

- “Finding small markets for energy solutions will be tricky—you could aim to replace diesel as a power source for remote islands, or maybe build modular reactors for quick deployment at military installations in hostile territories. Paradoxically, the challenge for the entrepreneurs who will create Energy 2.0 is to think small”