It always bothered me when I could not describe in simple words terms like public key, distributed ledger, trustless decentralized network, or compare how Bitcoin and the centralized banking system work without assuming any prior knowledge about either.

I have researched both systems and detailed my findings below.

Our current centralized financial system, with its tenets of a centralized database and of a trusted authority represented by a central bank, differs fundamentally from the Bitcoin decentralized network, which relies on math, computing resources and consensus to ensure that the incentives of the participants in the network and the security of the network are in complete alignment.

Recently, there has been much research and speculation as to whether banks should invest in the decentralized ledger technology to re-invent themselves in the digital age.

In response to that question, I argue that the decentralized ledger needs to be thought of as only a component of a decentralized payment network – such as Bitcoin, and thus the distributed ledger should not be regarded as a technology that could be separated from other operating principles of the Bitcoin decentralized network.

Consequently, banks, in partnership with innovative tech firms in the Bitcoin space, need to dedicate resources to examine how they can re-build their systems architecture on top of the Bitcoin decentralized network or other decentralized payment networks that have the same rewards/security governing-principle that the bitcoin network has.

I also detail how the Bank of England, KPMG, and the CEO of JP Morgan bank agree that the financial industry needs to look at Bitcoin as both an opportunity and a threat.

Centralized Banking System vs Decentralized Bitcoin Network

To understand the revolutionary premise behind the decentralized ledger, it would be important to compare how transactions take place under the current system, and how they do under the Bitcoin system.

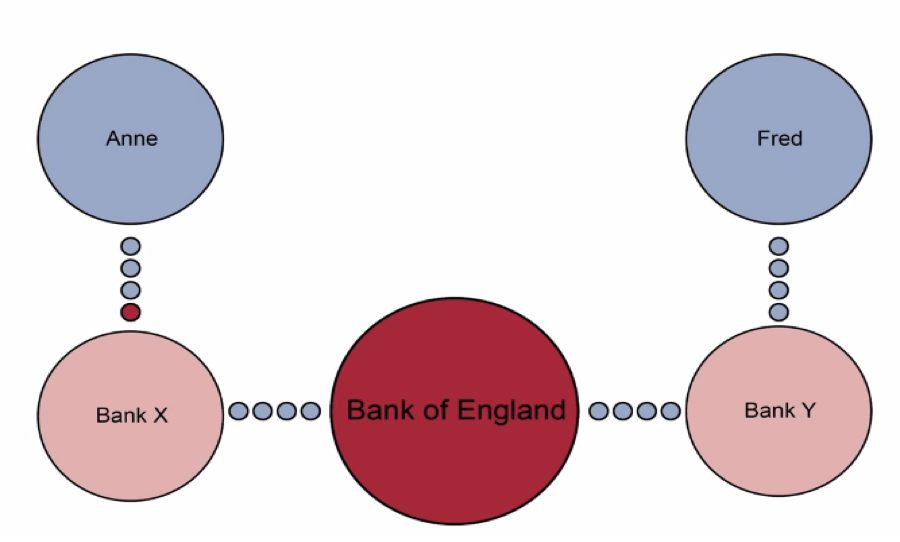

Architecture of The Current Financial System

Money, in essence, is a store of value denoted by banknotes and coins, and balances in bank accounts. These records were paper-based at some point in the past. However, our current banking system stores balances as digital records in a centralized computer. This digital record belongs to a bank. Any change to an account’s balance is nothing but an update to the data in the computer storing the data representing the account balance.

Under this system, transactions between banks are cleared through the central bank. If person A wants to transfer money to person B, that transfer would occur through the central bank – as seen below.

The central bank is needed to help address the following scenarios:

- The risk of a bank not having enough money to pay how much it owes other members of the system – insolvency.

- The risk of a bank not being able to have enough cash to cover withdraw request at a moment in time despite having money to cover all of its debts – solvent.

- Operational Risks such as IT risks in which one bank might become inaccessible on the network due lost connectivity.

- The central bank acts as a credible central authority in control of managing interactions among banks, each of which is required to maintain a deposit with the central bank to hedge against the risks they create in the network. (Ali, 2014)

Recent developments that came from within the banking system such as CIBC mobile payment(Canadian Imperial Bank of Commerce, 2015) reside on top of the architecture of the current system. Although a transaction is initiated through two mobile phones, the underlying process remains unchanged, for that banks sit one layer under these phones and perform the actual process of money transfer in the way explained above.

Architecture of The Bitcoin System – the Decentralized Ledger

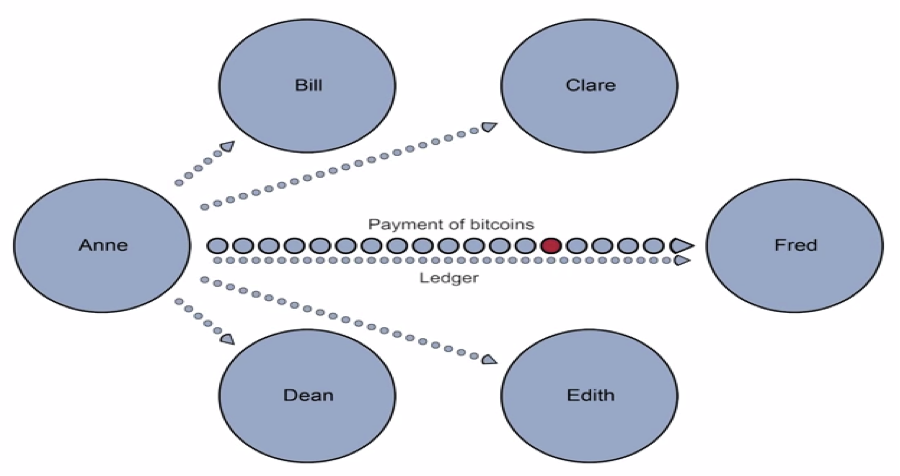

While Bitcoin is similar to the current banking system in that it also stores transactional data, it differs with the current system in how these records are maintained.

The Bitcoin network saves transactional records by creating a network of participants – nodes, all of which have the same role within the network – a decentralized network.

Each node is given two randomly generated mathematical numbers: One that serves as the identification address of the node on the network – public key, and the other one serves as a proof that the node owns any Bitcoins it sends. When nodes exchange Bitcoins on the network, and to eliminate the need for a trusted centralized entity, the node broadcasts, with each transaction, an up-to-date copy of the history of all Bitcoin transactions to date – the distributed ledger.

Bitcoin addresses security in two ways:

- Ensuring that the transaction is sent to the appropriate recipient by giving each participant a unique identifier on the network – an address or public key. When a transaction is broadcasted on the network, it would have the destination address in it so that the transaction can be accepted only by one node.

- Ensuring that the node initiating the transaction has ownership of the Bitcoins that they want to give to someone else and that they had received these Bitcoins voluntarily from someone else. This is done with an encrypted number – Private key, which is mathematically related to the public key. In order for that mathematical relationship to be proven, computing resources have to be committed to solve the mathematical equation –

- After the transaction conformation, the node that committed the resource to confirming the transaction gets awarded a unit of value –

The series of steps explained above is what makes a trustless and decentralized network like Bitcoin works. The incentives of the nodes are aligned by ensuring that the more they participate in maintaining the security of the network – through mining, the more get rewarded – in Bitcoins.

The diagram below offers a simplified diagram of how the Bitcoin network is structured in comparison with the traditional centralized financial system.

The above information, although somewhat technical, are essential in assessing the possibility of using the distributed ledger technology outside of the Bitcoin network by banks.

Can Banks Isolate The Distributed Ledger Aspect of The Bitcoin system and Build on Top of it?

The answer to this question becomes easier after understanding the role that each of the components of the Bitcoin network takes in ensuring the validity of the network itself.

The decentralized ledger is accurate because the majority of nodes in a decentralized network have the same exact copy of it. The nodes perform mathematical computational work – as explained earlier above, to ensure the accuracy of the ledger in terms of who legitimately owns which Bitcoins and what that amount is. These nodes are incentivized to devote computing resources to ensure the validity of the transactions by receiving rewards in return – Bitcoin.

Thus, a decentralized ledger could not exist outside of an incentive-based decentralized network.

Extensive research on this topic has shown that there is no entity that has provided the genesis of such a system. Some of my notable findings include:

- IBM/Samsung report: IBM stated in its report that it is possible to use the blockchain technology to build a decentralized network of the Internet of things. IBM indicates that “While the blockchain may carry regulatory and economic risk as a long-term store of value (as in the case of Bitcoin), it can be quite revolutionary as a transaction processing tool In our vision of a decentralized IoT, the blockchain is the framework facilitating transaction processing and coordination among interacting devices. Each manages its own roles and behavior, resulting in an ‘Internet of Decentralized, Autonomous Things’ – and thus the democratization of the digital world” (Paul Brody, 2014)

A demo video of a prototype device that IBM built – in collaboration with Samsung, shows that the underlying blockchain technology is actually an incentive-based decentralized network called Ethereum (TheProtocol.tv, 2015)

Ethereum is a proposed- has not been officially released yet, decentralized network and relies on mining – the concept of rewards, to maintain the blockchain (Leishman, 2015)

- The bank of England also suggested that the blockchain technology could become a revolutionary technology in maintaining digital records “The distributed ledger is a genuine technological innovation which demonstrates that digital records can be held securely without any central authority.”

It is important to clarify the statement of the Bank of England by indicating that a decentralized network is the genuine technical innovation, not the distributed ledger. The distributed ledger, in and of itself, is a very inefficient process to maintain digital records unless it is part of a completely open network where computer resources, committed by each node, counts.

- Recent news suggested that Infosys is looking into implementing the blockchain technology in its Finacle banking software. However, Infosys indicated that the company is still not certain how the technology will be implemented “The thing with this (Blockchain) is that we still do not know the full technology impact it can have.” (Andersen, 2015)

We can conclude from the above that an implementation of a truly decentralized ledger requires the implementation of all the elements that a fully decentralized network such as the one that Bitcoin offers.

Consequently, It would be important to look at the current limitations of the Bitcoin network.

Current Limitations of The Bitcoin Network

- Irrevocability of transactions and of private keys: When a transaction in the Bitcoin network occurs, it goes through a confirmation process – takes 10minutes. The result of that process is that the Bitcoin transaction is permanently added to the blockchain and can never be reversed.

This has serious implications for banks since they currently have a high degree of flexibility to reverse transactions for any reason – errors, fraud, contractual obligations, etc.

Private keys that can be thought of as a person’s wallet on the Bitcoin network are also impossible to recover once they are lost. To mask the complexity of the private key, and to reduce the difficulty of maintaining it by an individual, current Bitcoin wallet applications provide the user with a mnemonic phrase that is directly related to the private key. If that phrase is lost, so will be all the Bitcoins associated with the account. Again, the loss is permanent.

Currently, however, banks secure accounts by requiring owners to maintain a username and a password, which can be retrieved, or reset since the bank would have complete control over the information in the database.

- Ongoing development: The Bitcoin network is still relatively new. This results in instability in the space due to the network lack of exposure to world events and limitations that the centralized system has.

This lack of maturity represents an element of the risk of the unknown that could be devastating to banks should a serious flaw in the system get discovered at a later stage.

- Lack of adoption and price volatility: The volume of transactions on the Bitcoin network is currently very low when compared to other networks such as VISA (Bitcoin Wiki, 2014). Although the lack of adoption is a problem in and of itself, it also contributes to a related problem, which is price volatility.

Bitcoin price could be easily influenced – partly because of the current low adoption rate, and cause fluctuations in price that far outpace those of fiat currency – Bitcoin historically was 15 times more volatile than major fiat currencies. (Dourado, 2015).

It is easy to imagine the problems banks would have to deal with if the underlying currency they work with is that volatile. This would mean asset valuations, interest rates, commodity prices, growth forecasts, consumer confidence index, any many other aspects cannot be predicted with confidence.

This raises an important question: How should banks to the Bitcoin phenomena?

How Should Banks Respond to Bitcoin?

It would be helpful to look at what Bank of England, KPMG and the CEO of JP Morgan – the largest bank in the US, thought about this question.

The bank of England’s position can be summarized in the following statements:

- New technologies – such as the blockchain, take time until they show meaningful productivity improvement. The bank cites the example of electric motors, which took 30 years until the factories and the thought process that went behind manufacturing engines were fundamentally re-examined.

- Financial assets – such as loans and equity, are stored in digital records in a centralized database. Thus, the bank believes that it is conceivable that the current centralized infrastructure could give way to a decentralized structure in the future.

- The bank concludes by indicating that the impact of decentralized ledger would far pass the payment system, calling Bitcoin the “internet of finance”. (Ali, 2014)

KPMG, although focusing on different aspects of potential changes, still agreed in principle with the Bank of England’s vision about the impact Bitcoin can have.

- The auditing firm speaks of “an e-moment” for the banking industry similar to that of books when buying of digital books took off and the buying of paper-based books started declining at a comparable rate.

- KPMG indicates that banks did not experience any serious disruptions in the banking space in the past few decades, and that even the challenges encountered – such as the invention of ATM, was brought from players within the banking industry, unlike the case with Bitcoin. The firm argues that this is evidence that the banking industry is in need of radically re-thinking the potential changes occurring in the industry.

- KPMG describes Bitcoin as “internet of money” and adopts a balanced approach in describing how the decentralized digital currency could represent an opportunity for banks to capitalize on their resources and innovate or remain stifled in old ways of thinking and risk becoming irrelevant. (McCarthy, 2015)

In his letter to the shareholders, Jamie Dimon – the CEO of JP Morgan Chase, acknowledges the need for banks to learn from technologies such as Bitcoin “In terms of real-time systems, better encryption techniques, and reduction of costs and ‘pain points’ for customers” (Dimon, 2015).

The common theme from these findings is that the Bitcoin decentralized network represents a technology that banks can no longer ignore. Banks need to dedicate financial and human resources to building extensively researched models as to how best banks can react to the emergence of decentralized networks such as Bitcoin.

The following two examples provide a glimpse of the type of innovation that Bitcoin could bring to the banking system:

- Abra: This mobile application allows each person with a mobile phone to turn into a remittance service provider. A user – sender, can deposit money into her account through her mobile phone or by meeting another teller – another person on the same network. The sender initiates a send, and through the power of Bitcoin, the funds could be instantly available to another person, anywhere in the world, through a teller – who charges a fee. (DONNELLY, 2015)

- Chromaway: This company attempts to expand the role of Bitcoin to represent more than just a currency by adding additional information to the blockchain that can label certain Bitcoins as stocks, gold, or a deed to a building (Chromaway, 2014).

Conclusion

The mere fact that the Bitcoin innovation came from outside of the banking industry serves as a proof that it is time for banks to re-think some of the fundamental assumptions they have been operating under for the past few decades. While I cannot predict how the banking system will evolve or how Bitcoin will, banks need to invest resources and strategic teams into building future-scenarios as to how Bitcoin can influence the current banking system and what banks need to do to be ready should any of these scenarios pan out. In this respect, partnerships with technology companies – both in the Bitcoin and outside of the Bitcoin space, will be an essential strategy to ensure banks fast track and close the knowledge gap currently exists. Those banks that move first and commit the proper resources will immensely benefit in the long run.

References

Ali, R. (2014, 11 14). The emergence of digital currencies. Retrieved 4 12, 2015, from Bank of Engalnd: http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q3digitalcurrenciesbitcoin1.pdf

Andersen, M. (2015, Apr 13). Infosys looks to the future of Finacle with the Bitcoin blockchain. Retrieved Apr 20, 2015, from The Stack: http://thestack.com/infosys-finacle-blockchain-130415

Bitcoin Wiki. (2014, nov 8). Scalability. Retrieved apr 16, 2015, from Bitcoin Wiki: https://en.bitcoin.it/wiki/Scalability

Blockchain size. (2015, 04 20). Retrieved 04 16, 2015, from Blockchain: https://blockchain.info/charts/blocks-size

Canadian Imperial Bank of Commerce. (2015, 1 10). Mobile Payments. Retrieved 4 12, 2015, from CIBC: https://www.cibc.com/ca/features/mobile-payment.html

Chromaway. (2014, aug 21). Chromaway overview. Retrieved apr 15, 2015, from Chromaway: http://www.chromaway.com/#/overview

Dimon, J. (2015, apr 8). Letter to Shareholders. Retrieved apr 15, 2015, from JP Morgan Chase: http://files.shareholder.com/downloads/ONE/15660259x0x820077/8af78e45-1d81-4363-931c-439d04312ebc/JPMC-AR2014-LetterToShareholders.pdf

Dourado, E. (2015, apr 12). The Bitcoin Volatility Index. Retrieved apr 15, 2015, from The Bitcoin Volatility Index: https://btcvol.info/

DONNELLY, J. (2015, mar 5). Can Abra be Bitcoin’s Killer App. Retrieved apr 15, 2015, from The Bitcoin Magazine: https://bitcoinmagazine.com/19490/abra-announced-launch-festival-2015-seamless-remittances-powered-bitcoin/

Lee, T. (2013, Nov 13). The Switch. Retrieved Apr 20, 2015, from The Washington Post: http://www.washingtonpost.com/blogs/the-switch/wp/2013/11/12/bitcoin-needs-to-scale-by-a-factor-of-1000-to-compete-with-visa-heres-how-to-do-it/

Leishman, A. (2015, 03 01). A Next-Generation Smart Contract and Decentralized Application Platform. Retrieved 04 20, 2015, from Github: https://github.com/ethereum/wiki/wiki/White-Paper#blockchain-and-mining

McCarthy, R. (2015, jan 10). The changing World of Money. Retrieved apr 15, 2015, from KPMG: https://www.kpmg.com/UK/en/IssuesAndInsights/ArticlesPublications/Documents/PDF/Market%20Sector/Financial%20Services/the-changing-world-of-money.pdf

Paul Brody, V. P. (2014, sep 10). Device democracy, saving the future of the internet of things. Retrieved apr 15, 2015, from IBM: http://public.dhe.ibm.com/common/ssi/ecm/gb/en/gbe03620usen/GBE03620USEN.PDF

TheProtocol.tv. (2015, jan 13). ADEPT demo by IBM/Samsung. Retrieved apr 15, 2015, from TheProtocol.TV: https://www.theprotocol.tv/adept-demo-ibm-samsung/